Delivering Hyper-Personalization Within Insurance

What is Hyper-Personalization?

Hyper-personalization is the timely, relevant engagement of customers across all channels and at all stages of the lifecycle. This is driven by utilizing data, analytics, AI and automation to provide dynamic, personalized and targeted user experiences.

How Can Hyper-Personalization Impact Customer Growth?

Customer growth can be impacted in a number of ways, not just in the initial touchpoints of brand awareness and lead generation, but also during interactions with existing customers, tailoring the product offering to fit their needs and proactive management of renewals. Hyper-personalization unlocks value across all of these areas through a customer-centric, data-driven approach.

What is Hyper-Personalized Insurance?

Insurance companies have always offered a personalized service, as customers are offered policies at a particular price based on a measurement of risk. Personalization is also used in marketing to recommend certain products to certain customers. Hyper-personalization takes this further, bringing together a broader set of data (such as external and telemetry data) and using this to create a deeper and more dynamic understanding of the customer. This is then used to inform all aspects of customer engagement through digital and physical channels.

How Important Is Customer Growth in the Insurance Industry?

Insurers, re-insurers and brokers are increasingly focussed on how they can deliver more personalized, autonomous and tailored customer experiences. To meet this need, gaining a thorough understanding of every customer has never been more vital.

- Only 10% of organizations have explainable and trusted decision automation being used throughout the value-chain

- 70% of organizations lack a trusted holistic view of client across the enterprise

- Over 44% of the C-suite see a lack of trust in disparate data causing customer retention issues and missed customer opportunities

Most insurance executives have chosen AI, analytics, operational agility, and cloud as their top initiative priorities for the next two-three years. The need to be data-led and customer-centric is a challenge insurers, re-insurers and brokers are still trying to master, and existing MarTech and Customer Relationship Management (CRM) platforms lack the data fusion and analytics capabilities to solve these challenges.

The Challenges with Disconnected Data

Insurance companies face intense growth in regard to data complexity, evolving customer needs, challenging market conditions, and extreme competitiveness – which often hold them back.

Even with the scale of investment in data transformation, there are still multiple disparate and disconnect systems that hold and store customer information. This could be any combination of active policy data, historical quotes or claims, contact information, marketing preferences, engagement and web analytics data as well as insights derived from digital engagement and external sources. This disconnect in data leads to an unreliable and siloed view of customers across the business. This means that contact center agents, underwriters and claims handlers often have a vastly different analytical view of the same customer.

This challenge is exponentially compounded when you then look at the need to create low-touch processes through quoting and aggregation, payment verification, claims adjudication, chat bot customer servicing and the like.

There is a critical need for insurance organizations to extract more intelligence from their data and enrich this with external insights to improve their customer centric decision-making. Only then can organizations deliver greater customer value, increasing client retention and life-time value.

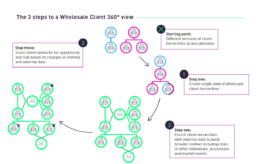

Use-Case of Hyper-Personalization in Insurance

Unlocking the value of customer data to generate a 360° view of customers will enable insurance organizations to reap the rewards that come with hyper-personalization through decision intelligence. For example, a Tier 1 client who deployed these capabilities was then able to:

- Generate over $200m additional revenue

- Leverage a 50% increase in the conversation rate of applications and tailored product offers

- Reduce prospecting time by 90%

- Provide decision automation by analyzing over ~60bn customer interactions & transactions

The Benefits of Decision Intelligence Across the Insurance Value Chain

Those organizations that can unlock a connected and enterprise-wide customer view, quickly analyze customer context and engagement information, as well as dynamically analyze customer relationships and interactions, are able to inform more appropriate next best actions for clients.

The activation of these insights can be delivered through any number of areas across the value-chain:

Customer Service

Faster, more appropriate and tailored service which empowers automated decisions but also omni-channel customer interaction

Cross-sell

Cross-sell - delivering warm and relevant leads for multi-product or multi-policyholder bundles and incentives

Claims

Claims – being able to more accurately segment claims for processing by not only reviewing the claim information, but by better understanding the customer, claimant, and supply chain behaviors.

Intelligent Underwriting

Intelligent Underwriting – automated and tailored ratings, pricing and distribution which better selects risk, and better protects the book

Digital Hyper-Personalisation

Digital Hyper-Personalisation – tailored, dynamic self-service that accurately reflects the customer engagement and needs

New Product Development

New Product Development – performing analytical testing of entire customer populations to stress test the network effect of new and evolving product lines for areas such as churn/retention modelling as well as loss propensity prediction.

Using Context to Drive Personalized Customer Experiences at Scale

The COVID-19 pandemic has forced companies around the globe to change their approach to managing customer relationships. Apart from shifting their employees to work remotely, they’ve had to rethink how to meet the needs of their customers in much the same way using digital customer experiences. Some companies have had to quickly transition their services to digital channels, while for others this period has brought increased scrutiny to the levels of personalized customer experience and service that can be provided through existing digital channels or accelerated digital transformation plans.

Hyper-Personalize your Insurance Company with CDI

Contextual Decision Intelligence (CDI) is changing the way carriers, re-insurers and brokers can seamlessly connect data from different sources, formats, and systems to provide accurate, dynamic, and connected 360° views of all customers, claimants, and third-parties in one place. This provides the context and the insight needed to drive true real-time hyper-personalized experiences to customers across all channels.

Drive Personalized Customer Experiences at Scale

Companies must not only ensure that new human-to-machine interactions are adequate replacements for the human-to-human relationships that customers are accustomed to provide a seamless customer experience, but they should also use this as an opportunity to invest in data platforms to drive intelligent customer engagement at scale.

This requires a layer of data intelligence that’s possible only through entity resolution, network generation and advanced analytics. Together, these critical elements connect a broad range of data to deliver deep insights, relevant prompts, and personalized content through digital channels straight to the client.

In this post, learn how to create a seamless, personalized customer experience in your digital channels. Find out the factors behind this push, common data challenges, why customer differentiation matters, and how to create that unique, customized experience that’s as engaging as being face-to-face.

Why Digital Customer Experiences are More Important Than Ever

Consumers’ increased use of digital channels has accelerated the need for large companies across all industries to invest more in their digital services. A few factors have triggered this push to digital customer experiences as shown below.

Generational influence

A more digital-savvy younger generation is driving organizations to meet their needs wherever they are with personalized customer experiences. Both as consumers and in taking on key roles in managing high-value areas in larger organizations, they realize how critical it is to cater to this audience.

Shift from face-to-face business transactions

The older, traditional, brick-and-mortar organizations suffer from fragmented operations, organizational silos, and legacy technology. They are being confronted with competitive pressure by the increase in digital-first or digital-only companies.

Lower cost of doing business

Moving business to digital channels lowers the cost of business operations. Instead of visiting a physical location, customers can log into a digital app or website to get the services they need at their fingertips. Online access to services also meets customers’ needs for immediacy and flexibility, creating a better overall customer experience.

Shift from face-to-face business transactions

To reduce transmission and infection from the COVID-19 virus, stay-at-home orders and social distancing guidelines went into effect. As a result, it forced businesses to close their doors to and restrict in-person interactions. This has accelerated the transition to digital channels, with McKinsey reporting a three to four-year acceleration of the digitization of customer interactions.

These newer online companies cater to a younger generation with their smooth-flowing online applications and better personal experiences. As a result, older financial organizations face trying to meet this challenge at the same level or better.

The Challenges of Connecting Customer Data

Digital servicing is not a new concept, and for decades organizations have been trying to provide the best possible experiences to their customers via website or mobile apps. This has involved the use of several types of technology, from Data Management Platforms to Content Management Systems and customer data platforms (CDPs). These platforms help organizations make sense of customer touchpoints and segment customers into groups that can be targeted with appropriate messaging or content. However, these platforms have some drawbacks, particularly in a B2B context, which prevent them from capitalizing on the opportunity to deliver 1-1 personalization at scale.

Lack of a single customer view

One of the most fundamental challenges in delivering seamless customer experiences is the lack of a reliable single customer view. For example, if you have a mortgage and checking account at your bank, you expect to log in and access both accounts as the same person. However, your bank may consider you as two different personas—one for each type of account. If you open a business account this may be considered separately again. This results in fragmented customer experiences across channels, products, and geographies.

Personalization based on partial information

Personalization is often driven based on a narrow view of digital and marketing data such as page views or campaign engagement. The use of a broader set of data enables more meaningful and tailored personalization, from external data such as news articles or reported financials to behavioral data from existing product utilization. However, this broader set of data is difficult to incorporate as it often lacks IDs or attributes that enable exact matching (such as IP addresses and emails), and therefore requires a more sophisticated matching approach.

Limited understanding of connections between users

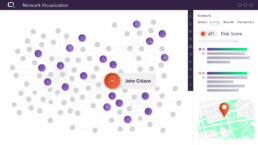

Understanding relationships between users brings an extra layer of context to improve the customer personalization experience. For example, where you have a B2B client with a complex structure and many users across various accounts each interacting with different channels, obtaining a holistic view of these client touchpoints can provide unique insights into patterns of interaction. This can support personalization on an individual user level but can also provide insights that inform more fundamental changes to service design. Existing tools lack the graph or network capabilities needed to build this relationship intelligence.

Need for a Differentiated Experience

Organizations need the ability to create a differentiated customer experience. Delivering this caliber of personalized customer experience requires data intelligence. With data intelligence, you can predict your customers’ interests and suggest the most relevant actions, products, or services they might need next. Here are a couple of reasons a differentiated experience is key to succeeding in a digital-first world.

Going beyond what’s expected

Organizations need to stand out against the competition, minimizing friction and creating memorable moments for their customers that drive brand advocacy.

Consider an individual who has recently started a new business but is yet to open a business account; they then receive a notification from their personal online banking app directing them to a catalog of useful information, products, and services for young and growing businesses. Or the administrator of a large business who is trying to contact their corporate mobile phone provider via a web portal and is intelligently routed directly to a human agent rather than an automated chatbot due to the high-value nature of the relationship – and following an earlier complaint made about the chatbot service. By creating these types of differentiated experiences, organizations can not only improve customer satisfaction and retention, but nurture and grow customer relationships.

Transition of intelligence

Consider the parts of your business that are more people intensive. For example, you might have several relationship managers who provide one-on-one care and attention to their clients. Increasingly, organizations are migrating some of those interactions toward digital channels.

To ensure customer satisfaction and provide the level of interaction they need, the intelligence behind that digital interface must try to replicate the intelligence of your relationship management team by understanding:

- The customer

- Their needs

- How to communicate and engage with them

- When to trigger proactive outreach

This level of understanding requires having the ability to intelligently connect and process the data to find insights. By using this approach, you can work with your customers in the best automated way possible through digital channels and reduce your reliance on customer-facing teams.

Drive contextual engagement for differentiated experiences in your digital channels with the customer intelligence platform from Nanogon.

How to Create a Seamless, Hyper-personalized Customer Experience

Apart from setting up a slick digital interface, seamless, personalized customer experiences are driven by intelligent data processing behind the scenes. Innovative solutions provide several advanced capabilities that can complement existing technologies and provide a step-change in value.

Entity resolution

With entity resolution, you create a single view of your customers and prospects from poor quality or sparse data. Through this process, you connect the data across your channels or touchpoints a customer might interact with and any broader firm-wide data. This goes beyond traditional matching and overcomes ambiguities in the data. For example, you can connect online portal behavioral data with product utilization data, finance data, and external data. By bringing that data together, you generate a complete view of each customer or potential customer.

Network generation

To build that broader context, you need the scalable graphing capabilities of network generation. Consider a couple of examples:

- One of your customers interacts regularly with your digital platform. You also know she’s a director of a particular business, so you might recommend insurance or other business products to her.

- A user belongs to an organization that is a subsidiary of a client that’s a major share of revenue for your organization. Rather than forcing them down a cumbersome customer journey, you’re able to make sure this customer gets the best experience possible.

In both examples, by using network generation, you create a greater context to instruct a more digital and personalized experience to further engage your customers.

Advanced Analytics

With access to artificial intelligence and machine learning, you apply advanced across those networks to automatically highlight opportunities where you can engage your customers. By using analytics, you move away from segmentation where customers must fit specific criteria, such as an age range or region. Instead, you create a segment of one where you process data about an individual and take a specific action based on that person’s profile, enabling a more personalized approach.

Areas to Unlock Business Value

When you build greater intelligence into the data framework behind your digital channels, you create a seamless customer journey and unlock value across a range of areas. Here are examples of just a few:

Holistic customer view

Know where your customers are on their journey. Maybe a customer can’t find what they need after logging into your web application and then switching to your mobile app. So, they call your service center. Based on the complete customer view, your service representative knows what your customer experienced before they called, understands what they need, and knows how to manage the interaction. Plus, your organization understands how it needs to update its systems to optimize its processes.

Hyper-personalized recommendations

Recommend specific products for a particular customer is great for personalized customer experiences. Consider a business customer, where analysis of accounts, payments, and supply chain data has indicated a potential working capital requirement. Relevant products can then be presented to this customer when they log in to manage their accounts.

Dynamic and real-time responses.

Score customer data in real time. When a customer completes your online form for a new loan, you know who the customer is, but also that they’re connected to a high-growing business and are a major shareholder. Because they’re probably good for the loan they applied for, you can respond dynamically to offer them a good rate. Auto-filled forms. Supply a seamless experience by auto-filling forms. Use the 360 views of internal and external data to make your customers’ lives easier by partially filling in forms the customer might be prompted to complete on your website or mobile app.

Proactive elements

Engage your customers right in your digital channels. When external data triggers news about a business, you can nudge customers about products or services related to that news, such as new investment products for shareholders of a company expected to IPO. You can proactively engage the customer right through your digital channels, instead of waiting for them to contact you.

Create More Personalization

When you connect your data across disparate internal and external sources using entity resolution, network generation, and analytics, you uncover greater decision intelligence. You generate real context around your customers to provide a deeper level of personalization. Plus, you differentiate your company light years over the competition.